A Semiconductor Industry Association (SIA)/Boston Consulting Group (BCG) study analyzes the benefits and vulnerabilities of the global semiconductor supply chain and recommends government actions to ensure its long-term strength and resilience. The report finds that while the current global semiconductor supply chain structure based on geographic specialization has enabled tremendous innovation, productivity, and cost savings over the last 30 years, new supply chain vulnerabilities have emerged that must be addressed by government actions, including funding incentives to boost domestic chip production and research.

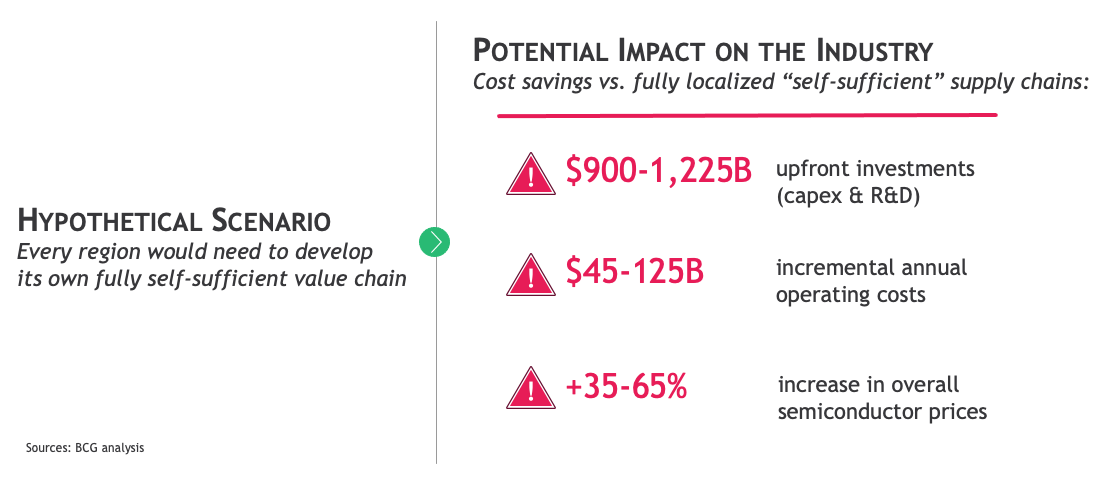

A hypothetical alternative with fully self-sufficient local supply chains in each region would require at least $1 trillion in incremental upfront investment and result in a 35% to 65% overall increase in semiconductor prices, ultimately resulting in higher costs of electronic devices for consumers.

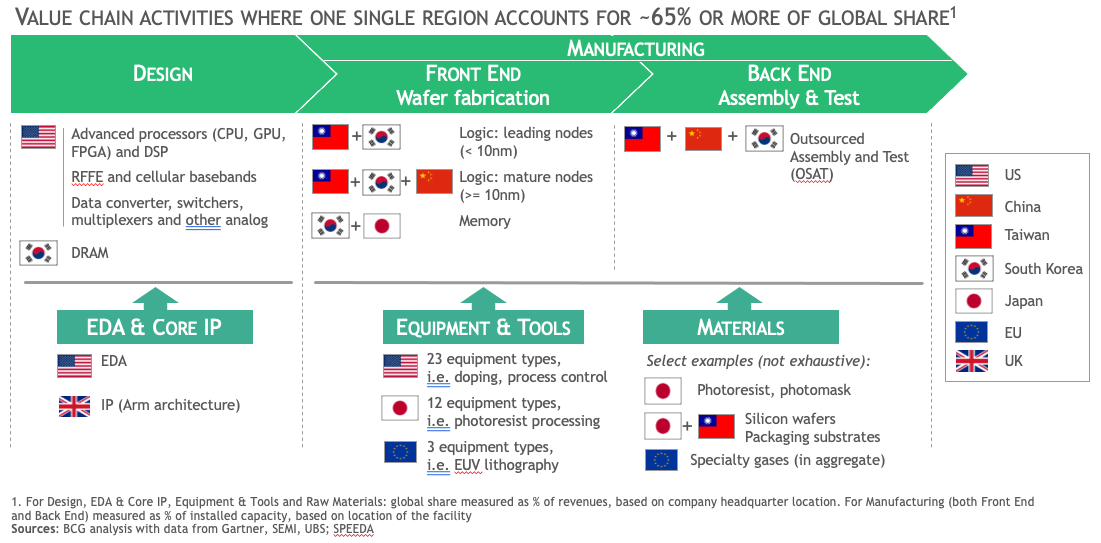

There are more than 50 points across the value chain where one region holds more than 65% of the global market share. These are potential single points of failure that could be disrupted by natural disasters, infrastructure shutdowns, or international conflicts, and may cause severe interruptions in the supply of essential chips. About 75% of global semiconductor manufacturing capacity, for example, is concentrated in China and East Asia, a region significantly exposed to high seismic activity and geopolitical tensions. In addition, 100% of the world’s most advanced (below 10 nanometers) semiconductor manufacturing capacity is currently located in Taiwan (92%) and South Korea (8%). These advanced chips are essential to America’s economy, national security, and critical infrastructure.

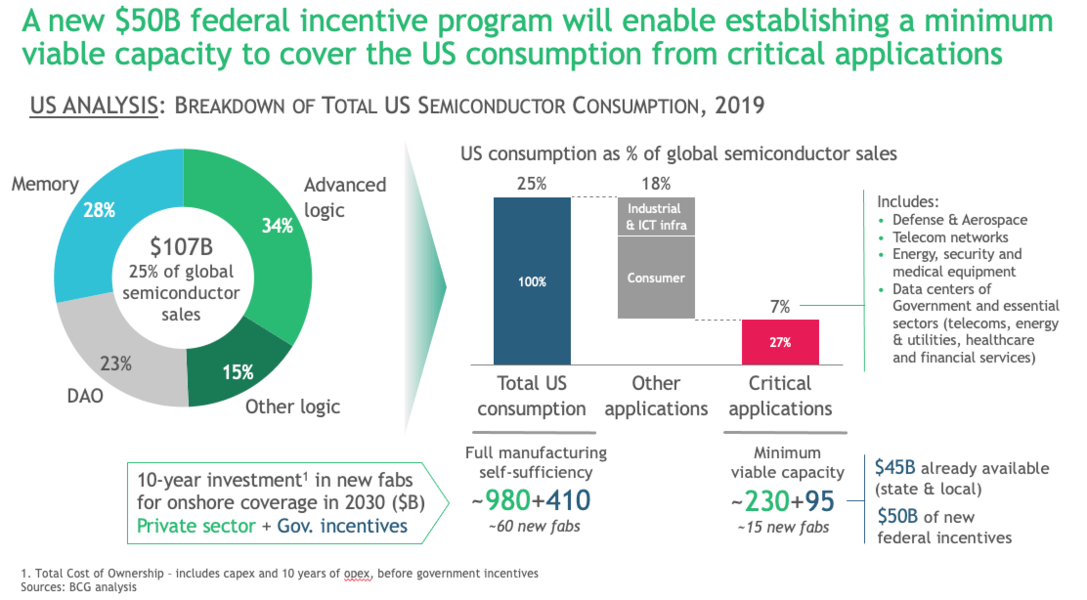

To reduce the risk of major global supply disruptions, the U.S. government should enact market-driven incentive programs to achieve a more diversified geographic footprint. These incentives should aim to expand semiconductor manufacturing capacity in the U.S. and broaden the supply of some critical materials. For example, the additional capacity from such incentives would enable the U.S. to meet domestic demand for advanced logic chips used in defense, aerospace, and critical infrastructure.